[Last updated: 1 January 2025, unless otherwise noted]

3.1 Shareholding rights and powers

The table below provides an overview of the different rights and powers that attach to different holding percentages in a listed corporation in Peru:

| Shareholding | Rights |

| One share |

|

| 5% or more (of existing share capital with right to vote) |

|

|

20% or more (of existing share capital with right to vote) |

|

|

25% (of existing share capital with right to vote) |

|

|

25% (of existing share capital with right to vote) |

|

|

33.33% |

|

|

40% (of existing share capital with right to vote) |

|

|

50% (of existing share capital with right to vote) |

|

|

50% + one share (represented at a general shareholders’ meeting) |

|

|

50% + one share (of existing share capital with right to vote) |

|

|

60% (of existing share capital with right to vote) |

|

|

66.66% (of existing share capital with right to vote) |

|

3.2 Restriction and careful planning

Peruvian law contains a number of rules that apply even before a public takeover bid is publicly announced. These rules impose restrictions and hurdles in relation to prior stake building by a bidder, announcements of a potential takeover bid or a target company, among others. The main restrictions and hurdles have been summarized below. Some careful planning is therefore necessary if a potential bidder or target company intends to start up a process intended at launching a public takeover bid.

3.3 Insider trading and market abuse

Any undisclosed public tender offer or the intention to launch a public takeover bid is deemed inside information by the Peruvian Securities Market Law and Market Abuse Regulations. Therefore, while the tender offer has not yet been announced to the market, all persons that have knowledge of it must refrain from misusing such information and keep that information strictly confidential. The Peruvian Securities Market Law and the Market Abuse Regulations consider that the information is misused when a person: (i) reveals the information to third parties, (ii) recommends operations to others based on such information, and (iii) uses the information to directly or indirectly benefit themself or third parties. In addition, such rules prohibit, among other things, manipulating the target’s stock price, e.g., by creating misleading rumors of a potential takeover bid.

3.4 Due diligence

Peruvian Tender Offer Regulations do not contain specific rules regarding whether or not a prior due diligence may be conducted, nor how such due diligence shall be conducted. Nevertheless, a prior due diligence or pre-acquisition review is generally accepted in practice (and by the SMV), and appropriate mechanisms have been developed to conduct a due diligence or pre-acquisition review and to mitigate potential market abuse and early disclosure concerns. These include the use of strict confidentiality procedures and data rooms.

3.5 Disclosure of shareholding

Although it is not standard practice for a Peruvian company to include a provision in its by-laws governing the ownership threshold above which share ownership must be disclosed. Under the current Economic Groups Regulations, listed companies must inform the SMV of the members of its economic group and a list of its holders of common shares that hold more than a 0.5% share interest, as well as any change to such information.

In addition, the Securities Market Law establishes that listed companies must inform the SMV and the Lima Stock Exchange of any transfer of its common shares made by any person or entity who directly or indirectly owns 10% or more of the company's total share capital or by any person or entity who directly or indirectly becomes owner of, or is no longer an owner of, 10% or more of the total share capital of a listed company.

3.6 The concept of "substantial interest"

The obligation to launch a tender offer is triggered when a person or group of persons (acting in concert) intends to acquire or has acquired a "substantial interest" in a target company (see 4 below). According to Peruvian Tender Offer Regulations, a substantial interest is acquired by a person or group of persons (acting in concert) when the purchase (i) will result in such person or group of persons (acting in concert) beneficially owning (directly or indirectly) at least 25% of the outstanding shares with voting rights of a company in one or a series of transactions, or (ii) allows such person to (a) appoint a majority of the directors of the target company or (b) amend the by-laws of the target company. Ownership thresholds of 50% and 60% also trigger certain rights to appoint a board member or control the company in general. When a person reaches or surpasses each of the 25%, 50% and 60% thresholds the obligation to launch a tender offer is triggered. This means that it is possible to move in between thresholds without triggering the obligation to launch a tender offer. For instance, if a person already owns 26% and increases its ownership to 47%, that will not trigger an obligation to launch a tender offer.

3.7 Calculation of indirect ownership

If an interest is acquired indirectly through an intermediate company, the following methods are used to determine whether the acquisition qualifies as an acquisition of substantial interest in the target company and, therefore, if such indirect acquisition triggers the obligation of the acquirer (or acquirers) to launch a subsequent mandatory tender offer or to otherwise sell the shares indirectly acquired in the target company.

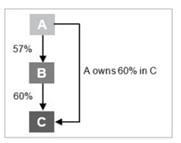

In cases where a person (A) acquires more than 50%, e.g., 57%, of the voting shares of an intermediate company (B), such person is deemed to acquire the percentage owned by the intermediate company (B), e.g., 60% in another company. This triggers the tender offer regulations in respect of the third company (C).

In cases where a person (A) acquires less than 50%, e.g., 23%, of the intermediate company (B), the indirect participation is calculated by multiplying such percentage by the percentage owned by the intermediate company (B), i.e., 76% in another company (C). This could trigger the tender offer regulations in respect of company C. In this example, company A does not meet the 25% threshold of outstanding shares with voting rights and, therefore, no mandatory tender offer would be triggered by company A in respect of either company B or company C.

3.8 Acting in concert

Pursuant to the Tender Offer Regulations, a person or group of persons acting in concert that acquires or intends to acquire a "substantial interest" (see 3.6) will be jointly liable to carry out a mandatory takeover bid, even though each individual group member does not surpass the required threshold to establish a "substantial interest" or otherwise have the power to (i) appoint a majority of the members of the target company's board of directors, or (ii) amend the by-laws of a target company.

3.9 Irrevocability

Peruvian laws provide that once the tender offer has been announced, such offer cannot be withdrawn, even in the case of a voluntary takeover bid.

3.10 Guarantees

An offeror must, prior to launching a bid, ensure that it will be able to fulfill its obligations in the offer by grating guarantees to secure the total amount of the consideration offered. If the consideration offered is (i) in cash or in securities to be issued by the target company or the offeror, as applicable, the guarantee must be granted for the total amount of such consideration and it may be in cash, a letter of credit or any other type of guarantee; provided, however, that such guarantee is unconditional, irrevocable and enforceable upon demand, and (ii) to be paid with previously issued securities, the offeror shall evidence that it is the legal owner of all the securities offered in exchange, and such securities are blocked in the account of the respective broker-dealer under which securities are registered or otherwise evidence that such securities will be available to pay the consideration offered in full.

3.11 Exemptions

There are a number of exceptions in which there is no obligation to launch a tender offer even though a substantial interest in a target company has been acquired. The main exemptions are the following:

- Prior written consent from all shareholders with a right to vote.

- When substantial interest is acquired as a consequence of a reorganization among companies of the same economic group, as long as such reorganization does not alter the ultimate control of the economic group.

- When substantial interest is acquired by a broker-dealer as a result of its fulfilment of an underwriting obligation.

- When shares are acquired by a depository for the purposes of subsequently issuing ADRs (American Depository Receipts), GDRs (Global Depository Receipts) or similar securities.

- When an ADR, GDR or similar security is acquired, unless the acquirer exercises the right to vote the underlying shares or requests delivery of such underlying shares.

- When substantial interest is acquired through an initial public offering.

- When substantial interest is acquired through a conversion of debt into capital stock under a bankruptcy procedure.

- When substantial interest is acquired through the exercise of pre-emptive rights.

- When substantial interest is acquired through the assignment of shares to a trust, as long as the trustee is a local financial entity or a foreign bank classified as a first in class by the Peruvian Central Bank and the trustor or originator maintains the right to vote of those shares.